The Australian share market is posting modest losses ahead of tomorrow's federal budget, forecasting weaker economic growth but a quicker return of inflation to the RBA's target range.

Follow the day's financial news and insights from our specialist business reporters on our live blog.

Disclaimer: this blog is not intended as investment advice.

Key events

To leave a comment on the blog, please log in or sign up for an ABC account.

Live updates

Market snapshot

- ASX 200: -0.2% to 7,732 points (live values below)

- Australian dollar: -0.1% to 65.95 US cents

- Nikkei: Flat at 38,244 points

- Hang Seng: +0.4% to 19,034 points

- Shanghai: -0.2% to 3,147 points

- S&P 500: +0.2% to 5,223 points (Friday)

- Nasdaq: flat at 16,341 points (Friday)

- FTSE: +0.6% at 8,434 points (Friday)

- EuroStoxx 600: +0.8% at 521 points (Friday)

- Spot gold: -0.1% to $US2,358/ounce

- Brent crude: -0.3% to $US82.52/barrel

- Iron ore: +0.2% to $US116.00/tonne

- Bitcoin: +0.9% to $US61,041

Prices current around 12:50pm AEST.

Live updates on the major ASX indices:

Federal government open to doing business again with scandal plagued PwC

Is the scandal plagued consulting firm PwC Australia about to be given a very satisfying Christmas present from the federal government?

Despite numerous inquiries into the firm's operations — including potential criminal behaviour by executives — it appears the government's freezer door has been left ajar for PwC Australia.

Daniel Ziffer has been digging around the issue and found not only had an agreement been reached between the Department of Finance and the company not to bid for any new work until December this year, but a subsidiary, partially owned by PwC, had just won a lucrative tax-payer funded contract.

It's a terrific read.

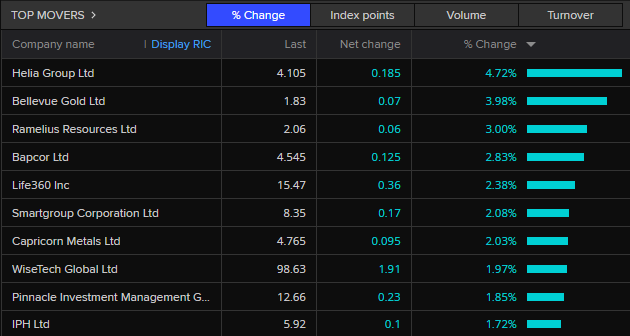

Big movers on ASX this morning

Top movers

Bottom movers

Note: ANZ went ex-dividend this morning

Business conditions ease, taking pressure off inflation: NAB

Business conditions have softened while confidence about future prospects held steady, according to the NAB monthly business survey.

The survey also found while overall profitability remained steady, key cost inputs such as labour and business purchases had eased.

The April reading of the mood of Australian business shows both confidence and conditions slipped back to their long-term trends, with the most notable move being a decline in the survey's employment index, although not into negative territory that would point to declining job numbers.

The survey found forward orders also fell in the month, driven by large movements in mining, manufacturing and construction, while the level of forward orders also remains negative in retail and wholesale.

NAB chief economist Alan Oster noted the most promising news in the survey was a sign of tentative easing in inflationary pressures.

"There was some further improvement in the pace of cost growth in April, as well as a step down in the pace of retail price growth after elevated readings in the first few months of the year," Mr Oster said.

"That is an optimistic sign for the prospects of some easing in inflation in Q2, though we will have to wait to see how this evolves over the coming months."

Update

- ASX200: -0.1% to 7,733 points

- Australian dollar: -0.3% at 66.01 US cents

- S&P 500: +0.2% to 5,223 points (Friday)

- Nasdaq: flat at 16,341 points (Friday)

- FTSE: +0.6% at 8,434 points (Friday)

- EuroStoxx 600: +0.8% at 521 points (Friday)

- Spot gold: +0.1% at $US2359/ounce

- Brent crude: -1.3% at $US82.79/barrel

- Iron ore: -1.6% $118.62/tonne

- Bitcoin: +1.7% to $US61,487.10

ASX down 0.3% on opening

The ASX has opened the week with more spills than thrills.

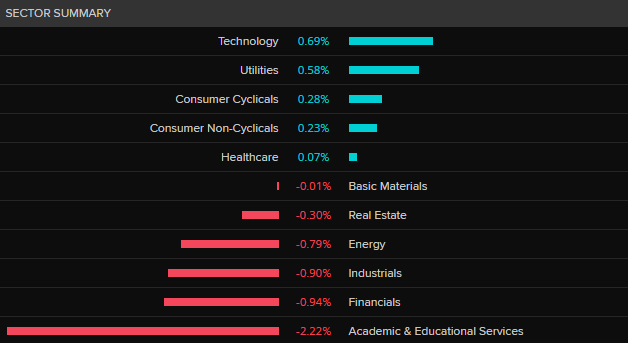

At 10:30am (AEST) it had slipped 0.3% with losses the in financial, industrial and energy sectors outweighing gains among technology and utility stocks.

US inflation the focus of global markets

Overseas the big number — although hopefully not too big — will be US inflation (Wednesday).

With US wage and jobs growth currently strong, the consensus is for another too-hot-for-comfort 0.3% jump in the CPI over the month.

"If the CPI report comes in hotter, it's going to likely price out any rate cuts for 2024," Matthew Miskin, co-chief investment strategist with John Hancock Investment Management told Reuters.

"You may actually have to start talking about policy that's more restrictive if (inflation) is too hot relative to expectations."

April's higher than expected CPI figures set US stocks back on their heels for a couple of weeks, another high figure could derail the current rally.

On Friday China has its big monthly data dump with industrial production, retail sales and fixed asset investment figures signed, sealed and delivered less than two weeks after the April deadline closed.

Federal budget to dominate the week

The federal budget on Tuesday evening will dominate the week in finance, although probably without overly influencing the market sentiment.

As is the norm these days, large chunks of the budget have been released already, but there's still plenty to come as Treasurer Jim Chalmers treads a fine line between the promised cost-of-living relief and firing up inflation (aka adding the risk of interest rate hikes).

A key figure will be whether there will be a deficit or surplus.

Treasury’s Mid-Year Economic and Fiscal Outlook forecast a deficit of $1.1 billion. The CBA's economic team says year-to-date data shows the budget running well ahead of that and a surplus of $15 billion is likely.

The CBA says that could allow for a "mildly stimulatory … overall setting of policy – but not enough to have a significant impact on the expected path of monetary policy".

Jobs and wages are the key local data releases of the week.

The Wage Price Index (Wednesday) is forecast to show wages up about 0.9% over the quarter and 4.2% for the year.

Jobs data for April (Thursday) is expected to show a rebound in employment after a fall in March, nevertheless, unemployment is forecast to tick up to 3.9%. The data has been volatile of late, so it will be tricky to read too much into the result.

NAB will release its well-regarded monthly survey of business conditions and confidence this morning.

Market snapshot

- SPI 200: -0.2% to 7,749 points

- Australian dollar: -0.3% at 66.01 US cents

- S&P 500: +0.2% to 5,223 points (Friday)

- Nasdaq: flat at 16,341 points (Friday)

- FTSE: +0.6% at 8,434 points (Friday)

- EuroStoxx 600: +0.8% at 521 points (Friday)

- Spot gold: +0.6%/ounce

- Brent crude: -1.3% at $US82.79/barrel

- Iron ore: -1.6% $118.62/tonne

- Bitcoin: +0.3% to $US60,978.10

ASX set for sluggish start as global markets near record

Good morning! I'm Stephen Letts from the ABC's business team, and along with Michael Janda and Kate Ainsworth, we'll be taking you through the day's play on the markets and in finance, and as always, aiming to make every post a winner.

The auspices are not brilliant, with the ASX futures pointing to a slight fall on opening (-0.2%) despite Wall Street finishing the week with its eighth gain on the trot.

To be precise, the Dow (+0.3%) and S&P 500 (+0.2%) were up on Friday, while the Nasdaq ended marginally in the red.

Europe’s Eurostoxx 600 (+0.8%) and the UK's FTSE (0.6%) both hit record highs, pushing the MSCI's all-country world index to within 0.2% of its record close.

The US dollar and key bond rates edged higher on expectations that April CPI data out this week would reveal a fourth consecutive month of stronger-than-expected inflation, a result that may well price out any rate cut in the US this year.

As the day rolls on, expect the slow drip, drip, drip of pre-budget releases to continue. We'll keep you updated.

So, sit tight, here we go for another week.