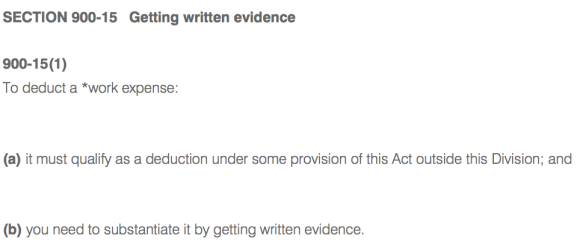

I have worked from home for over a decade. and I have always claimed my 52 cents for every hour I work. But now all the rest of you have joined me on the short morning walk from the kitchen to the desk… you get 80 cents and hour and I am stuck with my 52 cents…

Today the Commissioner updated the way we claim working from home expenses… he says there are three ways to calculate deductions for the running expenses of working at home:

- The fixed rate method – 52 cents per work hour for heating, cooling, lighting, cleaning and the decline in value of office furniture, plus the work-related phone and internet expenses ($50 a year as we have no records), consumables, stationery, and depreciation of a laptop .

- The actual cost method ─ claim the actual work-related portion of all your running expenses, which you need to calculate on a reasonable basis which is way to hard to work out.

- And now the shortcut method ─ claim a rate of 80 cents per work hour for all additional running expenses

Under this shortcut method taxpayers can claim a deduction of 80 cents for each hour they work from home due to COVID-19 as long as they are:

- working from home to fulfil your employment duties and not just carrying out minimal tasks such as occasionally checking emails or taking calls,

- incurring additional deductible running expenses as a result of working from home.

If a taxpayer uses the shortcut method, they cannot claim a further deduction for anything else, including the depreciation of their laptop.

They must keep a record of the number of hours they have worked from home as a result of COVID-19. Examples are timesheets, diary notes or rosters.

If they use the shortcut method to claim a deduction they must include the note ‘COVID-hourly rate’ in their tax return.

So poor me… I don’t work from home due to COVID-19 but because I am slack and lazy, so I just get the 52 cents and hour…

Update – The Commissioner has released a Practical Compliance Guideline with some examples.

Example 1 – not working from home

13. Abed’s employer has requested staff take leave while the business is suffering a turndown due to COVID-19. Abed takes four weeks annual leave. During that period he occasionally checks his email to see if there is anything he needs keep abreast of while he is on leave. His employer also sends him text messages to keep him up to date on changes to the business.

14. This would not qualify as working from home as Abed is on leave and not actively working; he is just occasionally checking in. As such, Abed cannot rely on this Guideline.

Example 2 – working from home

15. Bianca is a sole trader who works as a copy writer and editor. She usually works out of a shared workspace in the central business district as it is easier to meet with her clients face-to-face. Bianca decides to work from home as a result of COVID-19 and replaces her face-to-face meetings with online video conferencing. Bianca continues to operate her business and would meet the criteria for working from home. As such, Bianca can rely on this Guideline to claim her additional running expenses.

Example 4 – additional running expenses incurred – business owner

23. Elizabeth runs a small business selling art and framing pictures. She has a store with a workshop to display the art and frames. She also does all her bookkeeping and administrative tasks in the office at the store. As a result of the downturn in people coming into her store due to COVID-19, Elizabeth decides to close her store and continue running her business online from home. As Elizabeth continues to run her business from home due to COVID-19, she can rely on this Guideline to claim her additional running expenses.

Example 5 – calculating additional running expenses using shortcut rate

30. Ephrem is an employee and as a result of COVID-19 he is working from his home office. In order to work from home, Ephrem purchases a computer on 15 March 2020 for $1,299. He intends to use the shortcut rate to claim his additional running expenses.

31. During the entire period he is working from home as a result of COVID-19, Ephrem notes in the calendar on his computer, when he starts and finishes each day along with a note about any breaks he has and how long those breaks were.

32. When it comes to lodging his 2019-20 tax return, Ephrem works out that during the period he worked from home as a result of COVID-19, he worked a total of 456 hours.

33. Ephrem calculates his deduction for the 2019-20 income year for additional running expenses as:

456 hours × 80 cents per hour = $364.80

34. As Ephrem has claimed his additional running expenses using the shortcut rate, he cannot claim a separate deduction for the decline in value of his computer. Ephrem keeps a record of the calendar entries he has made to demonstrate how he calculated the number of hours he worked from home. Ephrem also keeps the receipts for his computer purchase in case he will need to claim depreciation in future.

35. When he lodges his 2019-20 tax return using myGov, Ephrem includes the notation ‘COVID-hourly rate’.