Mainstream monetary theory — neat, plausible, and utterly wrong

from Lars Syll

In modern times legal currencies are totally based on fiat. Currencies no longer have intrinsic value (as gold and silver). What gives them value is basically the legal status given to them by government and the simple fact that you have to pay your taxes with them. That also enables governments to run a kind of monopoly business where it never can run out of money. Hence spending becomes the prime mover and taxing and borrowing is degraded to following acts. If we have a depression, the solution, then, is not austerity. It is spending. Budget deficits are not the major problem, since fiat money means that governments can always make more of them.

Financing quantitative easing, fiscal expansion, and other similar operations, is made possible by simply crediting a bank account and thereby – by a single keystroke – actually creating money. One of the most important reasons why so many countries are still stuck in depression-like economic quagmires is that people in general – including most mainstream economists – simply don’t understand the workings of modern monetary systems. The result is totally and utterly wrong-headed austerity policies, emanating out of a groundless fear of creating inflation via central banks printing money, in a situation where we rather should fear deflation and inadequate effective demand.

Brexit, don’t forget how we got here

from Jamie Morgan

Understanding Brexit requires us to consider the political economy of tax justice and the abuse of wealth protection.

At a time when a general election has dominated the press for the last two months and Brexit has been a shadow of anxiety – a most remarkable event that the political parties have been steadfastly refusing to remark upon in any meaningful way – it is important to recall just how we got to the current state of affairs; a state that Craig Berry refers to as ‘undemocracy’. A narrow majority decision based on (at best) limited information has become a fait accompli empowering government to pursue a position regarding which the populous are still in ignorance. It is difficult to see what kind of mandate follows from this, but it is not difficult to see that the longstanding problem is one of increasing separation between citizenry and those who they elect to represent them.

Disintegration, distrust and any number of additional alliteratively phrasable and parsable terms and concepts have general and specific causes. If we are to understand how we got here there is a political economy to be considered. Financialisation has also meant the accumulation of financial assets creating wealth stocks and income flows for the few far more than for the many. Inequality is a process based on asymmetrical ownership of such assets. This has been both a product of and a contribution to the difference between a 1% and the 99%. Read more…

What do unions do?

from David Ruccio

When I ask my students that question, they don’t really have an answer. That’s because, like much of the rest of the U.S. population, they don’t have much experience with unions, either directly or indirectly—not when the union membership rate has fallen to below 11 percent nationwide and is only 6.4 percent in the private sector. Read more…

Do you want to get a Nobel prize? Eat chocolate and move to Chicago!

from Lars Syll

As we’ve noticed, again and again, correlation is not the same as causation …

If you want to get the prize in economics — and want to be on the sure side — yours truly would suggest you complement your intake of chocolate with a move to Chicago.

Out of the 78 laureates that have been awarded “The Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel,” 28 have been affiliated to The University of Chicago — that is 36%. The world is really a small place when it comes to economics …

Bread and roses

from David Ruccio

Mainstream economists and politicians have answers for everything.

Lose your job? Well, that’s just globalization and technology at work. Not much that can be done about that.

And if you still want a job? Then just move to where the jobs are—and make sure your children go to college in order to prepare themselves for the jobs that will be available in the future.

The fact is, they’re not particularly good answers. And people know it. That’s why working-class voters are questioning business as usual and registering their protest by supporting—in the case of Brexit, the 2016 U.S. presidential election, the 2017 snap election in Britain, and so on—alternative positions and politicians. Read more…

Links. High powered money in Greece, ECB transparancy reveales raw power, 50 years ago the Bundesbank combatted trade surpluses

High powered money in Greece. The EU is re-financing 8,5 billion of Greek debt. About 7 billion of this is just trading in one kind of government bonds for another kind of government bonds. Much ado about less than nothing. There is some welcome softening of the terms – but not enough. However: About 1,6 billion has to be used to pay overdue bills which have to be paid by the government. This exchanging private debt for government bonds and will lead to an injection of highly powered money into the Greek economy which will prevent bankruptcies, which will enable these suppliers to pay their bills to their suppliers. Spain has however already threatened to block the agreement as it wants to protect a corrupt Spanish citizen in charge of privatization in Greece.

The ECB doubles down on monetary financing of the government. The European Central Bank published a report detailing why banks do or do not get ELA (Emergency Liquidity Assistance). Read more…

The Republican thieves who stole health care

from Dean Baker

In their desperation to provide $600 billion in tax cuts to their rich campaign contributors, the Republicans have decided to abandon all the standard rules by which Congress has governed itself. The actions might seem extraordinary, but we know how desperately the richest people in the country need tax cuts, so who can complain if the normal procedures are not being followed?

Unfortunately the debate over the “repeal and replacement” of Obamacare is being confused with a debate over health care. Paul Ryan, Mitch McConnell and the rest of the Republican caucuses in the House and Senate don’t give a damn about health care. This is about getting $600 billion in tax cuts for the people who pay for their campaigns and will offer them jobs as high paid lobbyists when they leave office. The fact that the tax cuts are associated with health care for tens of millions of people is just a coincidence.

If anyone thought the Republicans were interested in actually putting together a health care plan that was better than Obamacare, their actions show beyond any doubt this is not the case. After the Congressional Budget Office (CBO) projected that the first version of the American Health Care Act (AHCA) would increase the number of people without insurance by 24 million, the Republican leadership rushed a vote of the revised version before CBO had time to evaluate it. Read more…

Leontief on the dismal state of economics

from Lars Syll

Much of current academic teaching and research has been criticized for its lack of relevance, that is, of immediate practical impact … I submit that the consistently indifferent performance in practical applications is in fact a symptom of a fundamental imbalance in the present state of our discipline. The weak and all too slowly growing empirical foundation clearly cannot support the proliferating superstructure of pure, or should I say, speculative economic theory …

Uncritical enthusiasm for mathematical formulation tends often to conceal the ephemeral substantive content of the argument behind the formidable front of algebraic signs … In the presentation of a new model, attention nowadays is usually centered on a step-by-step derivation of its formal properties. But if the author — or at least the referee who recommended the manuscript for publication — is technically competent, such mathematical manipulations, however long and intricate, can even without further checking be accepted as correct. Nevertheless, they are usually spelled out at great length. By the time it comes to interpretation of the substantive conclusions, the assumptions on which the model has been based are easily forgotten. But it is precisely the empirical validity of these assumptions on which the usefulness of the entire exercise depends.

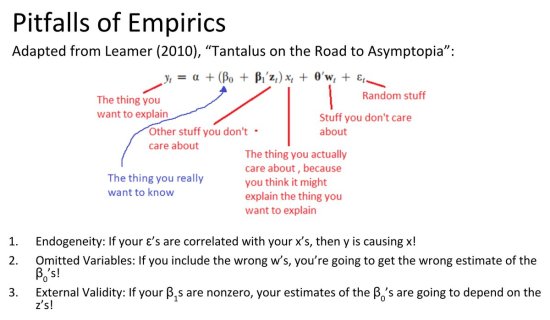

Ed Leamer and the pitfalls of econometrics

from Lars Syll

Ed Leamer’s Tantalus on the Road to Asymptopia is one of my favourite critiques of econometrics, and for the benefit of those who are not versed in the econometric jargong, this handy summary gives the gist of it in plain English:

Most work in econometrics and regression analysis is — still — made on the assumption that the researcher has a theoretical model that is ‘true.’ Based on this belief of having a correct specification for an econometric model or running a regression, one proceeds as if the only problem remaining to solve have to do with measurement and observation. Read more…

American myth

from David Ruccio

One of the most pernicious myths in the United States is that higher education successfully levels the playing field across students with different backgrounds and therefore reduces wealth inequality.

The reality is quite different—for the population as a whole and, especially, for racial and ethnic minorities. Read more…

Trumponomics: Causes and Consequences

paperback now available from the Amazon pages listed below

The counterintuitive problem

from Edward Fullbrook

Scientific education entails taming the authority of one’s intuition. Responsible citizenship in a democracy may entail it as well.

Keynes argued that markets often create inaccurate expectations of economic reality which people then act upon thereby changing reality. This reflexivity that Keynes identified as central to capitalist markets is the opposite of the basic process described by traditional economic theory, both in Keynes’ day and in our own, whereby it is assumed that market expectations are determined by market reality rather than one of that reality’s determinants.

For most people Keynes’ theory of market expectations, like his theory of aggregate demand, is counterintuitive, and therefore difficult to elucidate and popularize sufficiently to become part of public discussion. That is why George Soros’s role as a populariser of Keynes’ theory of expectations is potentially significant. It is my view that in democratic societies the ultimate obstacle to implementing and maintaining laws and policies that will make their economies function reasonably well and fairly is the challenge of intellectually enabling their populations, especially their pundits and politicians, to comprehend the counterintuitive dimensions of economic reality. Without that comprehension democratic societies will always be highly vulnerable to accepting the advice that follows from economic reasoning that excludes counterintuitive propositions and that serves the interests of tiny but powerful minorities.

Solow being uncomfortable with ‘modern’ macroeconomics

from Lars Syll

So in what sense is this “dynamic stochastic general equilibrium” model firmly grounded in the principles of economic theory? I do not want to be misunderstood. Friends have reminded me that much of the effort of “modern macro” goes into the incorporation of important deviations from the Panglossian assumptions that underlie the simplistic application of the Ramsey model to positive macroeconomics. Research focuses on the implications of wage and price stickiness, gaps and asymmetries of information, long-term contracts, imperfect competition, search, bargaining and other forms of strategic behavior, and so on. That is indeed so, and it is how progress is made.

But this diversity only intensifies my uncomfortable feeling that something is being put over on us, by ourselves. Why do so many of those research papers begin with a bow to the Ramsey model and cling to the basic outline? Every one of the deviations that I just mentioned was being studied by macroeconomists before the “modern” approach took over. That research was dismissed as “lacking microfoundations.” My point is precisely that attaching a realistic or behavioral deviation to the Ramsey model does not confer microfoundational legitimacy on the combination. Quite the contrary: a story loses legitimacy and credibility when it is spliced to a simple, extreme, and on the face of it, irrelevant special case. This is the core of my objection: adding some realistic frictions does not make it any more plausible that an observed economy is acting out the desires of a single, consistent, forward-looking intelligence …

For completeness, I suppose it could also be true that the bow to the Ramsey model is like wearing the school colors or singing the Notre Dame fight song: a harmless way of providing some apparent intellectual unity, and maybe even a minimal commonality of approach. That seems hardly worthy of grown-ups, especially because there is always a danger that some of the in-group come to believe the slogans, and it distorts their work …

There has always been a purist streak in economics that wants everything to follow neatly from greed, rationality, and equilibrium, with no ifs, ands, or buts. Most of us have felt that tug. Here is a theory that gives you just that, and this

time “everything” means everything: macro, not micro. The theory is neat, learnable, not terribly difficult, but just technical enough to feel like “science.”

Going private: the Trump administration’s big infrastructure plan

from Dean Baker

The Trump administration’s “infrastructure week” ended whatever hope any of us had that something positive could come out of this administration. It’s clear that his promise for rebuilding the country’s infrastructure is just another Trump scam.

During his campaign, Trump had made a point of complaining about the poor state of the country’s infrastructure. He had a point, as both the federal and state and local governments have cut back spending in recent years.

In the case of state and local governments, there was often little choice. Loss of tax revenue due to the recession and slow recovery, coupled with balanced budget requirements in state constitutions and city charters, meant that there was little money to spend.

In the case of the federal government, the deficit hawks insisted that we reduce the deficit, even though there is no evidence that high deficits are pushing up interest rates and/or leading to inflation. Interest rates continue to be extraordinarily low in both real and nominal terms. In fact, they were far lower in the late 1990s when the federal government was running budget surpluses.

Inflation continues to run below the Federal Reserve Board’s 2 percent target. In fact, the last few months it appears to be slowing slightly. Given this evidence, there seems little basis for the concern that budget deficits are too large.

Nonetheless, the domestic discretionary share of the budget, which includes everything from education to the Justice Department to infrastructure and public spending on medical, and other research, was cut back sharply by the deficit hawks. Read more…

The productivity stagnation – not a global phenomenon.

Long story short: labor productivity, as economists define it, is best understood as the amount of ‘stuff’ the income (wages, profits, rents, interest) related to one hour of work can buy (this is a somewhat idiosyncratic take on productivity. Look however here). Productivity is, as economists define it, not any kind of physical entity. It is supposed to be ‘value added’, or total income cq. the nominal value of net production, per hour of work. For about two centuries, give or take some decades, productivity has increased. Not anymore. At least: in a whole bunch of seemingly quite distinct countries (graph 1). This is, in a historical sense, really surprising. And economists spend a lot of ink about it: why did this happen? Which disease, nay, evil!, did beset the western economies! And it does require explanation. For any kind of explanation, however, we still need a more general picture of productivity developments in rich countries (I first wanted to include Japan in graph 1, too, but it turned out that Japanese productivity growth, though low, is clearly superior to these countries). Graph 2 shows developments in most of Europe.

Capital’s rising shares

from David Ruccio

Recently, I showed that conventional thinking about factor shares has been finally overturned: they are not necessarily constant, especially within existing economic institutions.

In fact, labor’s shares have been declining for decades now.

The opposite is true of capital’s shares: they’ve been rising for almost three decades. Read more…

Economics textbooks transmogrifying truth — wages and unemployment

from Lars Syll

A couple of weeks ago yours truly was sent a copy of the new edition of Chad Jones intermediate textbook Macroeconomics (4th ed, W W Norton, 2018). There’s much in the book I like, e. g. Jones’ combining of more traditional short-run macroeconomic analysis with an accessible coverage of the Romer model — the foundation of modern growth theory — and DSGE business cycle models.

A couple of weeks ago yours truly was sent a copy of the new edition of Chad Jones intermediate textbook Macroeconomics (4th ed, W W Norton, 2018). There’s much in the book I like, e. g. Jones’ combining of more traditional short-run macroeconomic analysis with an accessible coverage of the Romer model — the foundation of modern growth theory — and DSGE business cycle models.

Unfortunately it also contains some utter nonsense!

In chapter 7 — on “The Labor Market, Wages, and Unemployment” — Jones writes (p. 184):

The point of this experiment is to show that wage rigidities can lead to large movements in employment. Indeed, they are the reason John Maynard Keynes gave, in The General Theory of Employment, Interest, and Money (1936), for the high unemployment of the Great Depression.

A serious editor — who really checked the facts — would immediately find that although Keynes in General Theory devoted substantial attention to the subject of wage rigidities, he certainly did not hold the view that wage rigidities were “the reason … for the high unemployment of the Great Depression.” Read more…

The evidence does not support Macron’s claim that deregulating labor market will boost economy

from Dean Baker

In her Washington Post column, Catherine Rampell repeats some ill-founded conventional wisdom in telling readers that French president Emmanuel Macron’s plans to weaken labor unions and reduce restrictions on laying off workers are the path to revitalizing France’s economy. In fact, this claim is not supported by the evidence. There is little evidence that strong unions or labor market protections are associated with high unemployment.

The most obvious reason that France has had high unemployment is the turn to austerity in 2010 following the economic crisis. As a result of the cutbacks in government spending, there was no source of demand to replace the demand generated by asset bubbles prior to the crisis. For some reason, this fact is rarely mentioned in reporting on France’s economy.

It is also worth noting that France’s “stagnant labor market” has a much higher employment rate for prime age (ages 25 to 54) workers than the U.S. labor market (79.7 percent in France compared to 78.2 percent in the United States). This fact would seem to undermine the case that regulations are seriously hampering France’s labor market.

‘Cauchy logic’ in economics

from Lars Syll

What is 0.999 …, really? Is it 1? Or is it some number infinitesimally less than 1?

The right answer is to unmask the question. What is 0.999 …, really? It appears to refer to a kind of sum:

.9 + + 0.09 + 0.009 + 0.0009 + …

But what does that mean? That pesky ellipsis is the real problem. There can be no controversy about what it means to add up two, or three, or a hundred numbers. But infinitely many? That’s a different story. In the real world, you can never have infinitely many heaps. What’s the numerical value of an infinite sum? It doesn’t have one — until we give it one. That was the great innovation of Augustin-Louis Cauchy, who introduced the notion of limit into calculus in the 1820s.

The British number theorist G. H. Hardy … explains it best: “It is broadly true to say that mathematicians before Cauchy asked not, ‘How shall we define 1 – 1 – 1 + 1 – 1 …’ but ‘What is 1 -1 + 1 – 1 + …?’”

No matter how tight a cordon we draw around the number 1, the sum will eventually, after some finite number of steps, penetrate it, and never leave. Under those circumstances, Cauchy said, we should simply define the value of the infinite sum to be 1.

I have no problem with solving problems in mathematics by ‘defining’ them away. But how about the real world? Maybe that ought to be a question to ponder even for economists all to fond of uncritically following the mathematical way when applying their mathematical models to the real world, where indeed “you can never have infinitely many heaps” … Read more…

Pulling away

from David Ruccio

Apparently, Richard Reeves is worried that the top echelons of the U.S. middle class—those earning over $120,000—are separating from the rest of the country, and pulling up the drawbridge behind them.

“The upper middle class families have become greenhouses for the cultivation of human capital. Children raised in them are on a different track to ordinary Americans, right from the very beginning,” he writes.

The upper middle class are “opportunity hoarding” – making it harder for others less economically privileged to rise to the top; a situation that Reeves says places stress on the efficiency of the US economic system and creates dynastic wealth and privilege of the kind the nation’s fathers sought to avoid.

Recent Comments