When Ian Wilson was offered consumer protection insurance as an add-on to a personal loan in 2006, he thought it could be worthwhile if he ever lost his job.

Stepping out of the workforce in 2014, while suffering anxiety and depression, Mr Wilson decided to make a claim to support him in his time off.

More BusinessDay Videos

- Video duration

- 02:14

How does the insurance industry prepare ...

How does the insurance industry prepare for climate change?

Elizabeth Bryan, chairman of the Insurance Australia Group, talked up the need for infrastructure investment in communities before damaging climate change related weather events happen on Wednesday's Australian Financial Review & J.P Morgan Chanticleer lunch.

Up Next

Listed investment company skulduggery

- Video duration

- 02:25

- Video duration

- 02:25

Listed investment company skulduggery

Listed investment company skulduggery

Strange things are going on at Contango Microcap. Michael Pascoe comments.

Up Next

Yahoo CEO Marissa Mayer loses bonus

- Video duration

- 02:59

- Video duration

- 02:59

Yahoo CEO Marissa Mayer loses bonus

Yahoo CEO Marissa Mayer loses bonus

A Yahoo independent committee finds certain senior executives didn't properly "comprehend or investigate" a 2014 security breach.

Up Next

Will Snap make a successful IPO?

- Video duration

- 01:29

- Video duration

- 01:29

Will Snap make a successful IPO?

Will Snap make a successful IPO?

Examining Snapâs unique shareholder structure that may raise questions for investors in the long run.

Up Next

ASIC takes aim at the banks

- Video duration

- 01:08

- Video duration

- 01:08

ASIC takes aim at the banks

ASIC takes aim at the banks

ASIC chairman Greg Medcraft tells the Economics Legislation Committee bank culture is still an issue that needs to be addressed.

Up Next

Chinese billionaires gain most from Trump effect

- Video duration

- 02:39

- Video duration

- 02:39

Chinese billionaires gain most from Trump ...

Chinese billionaires gain most from Trump effect

How Chinese and Mexican billionaires have fared on the Bloomberg Billionaires Index since rPresident Trump entered the White House.

Up Next

Angry Caltex franchisees protest

- Video duration

- 01:53

- Video duration

- 01:53

Angry Caltex franchisees protest

Angry Caltex franchisees protest

A group of disgruntled Caltex service station owners have lead a protest through the streets of Sydney, calling for a more equitable business model.

Up Next

YouTube CEO sees huge opportunity

- Video duration

- 05:48

- Video duration

- 05:48

YouTube CEO sees huge opportunity

YouTube CEO sees huge opportunity

Susan Wojcicki discusses the company's new service, YouTube TV.

How does the insurance industry prepare for climate change?

Elizabeth Bryan, chairman of the Insurance Australia Group, talked up the need for infrastructure investment in communities before damaging climate change related weather events happen on Wednesday's Australian Financial Review & J.P Morgan Chanticleer lunch.

What followed was a seven-month battle with his insurance provider to have his claim acknowledged.

"When I originally looked at the product disclosure statement [PDS], I scanned over it and everything seemed reasonable. But then when I found out what I was getting knocked back for, I couldn't understand," he said.

Mr Wilson's claim was initially knocked back because there was one week in between leaving his position at a bank and seeing his doctor, who determined he was unfit for work.

"They would have been happy if I went to the doctor and then resigned one day after. But because I stopped work and saw the doctor one week later I was excluded."

His provider also relied on an exclusion listed in the PDS, that he would not be covered for "disturbance to mind or faculty through the use of alcohol and/or drugs", a finding he disputed and which was later proven untrue by an additional report from his doctor.

"I worked for a bank, so I know how to read these things, but for the general consumer I find the PDS uses ambiguous language ... and I feel a lot of these insurance companies hide behind the legal jargon," he said.

"I suppose how I'd like to see it as a consumer, is including the legal terms, but then in brackets something in plain language about what they mean."

While his claim was eventually successful, Mr Wilson said he was disappointed that he had to seek legal advice in order to achieve a result.

The frequency of consumer experiences like Mr Wilson's was the focus of recent research from the Insurance Council of Australia's Effective Disclosure Task Force.

It found that while 88 per cent of 2430 surveyed consumers said they had a confident understanding of their policy, when tested, their understanding of policy exclusions and limits was "poor".

It found that while 88 per cent of 2430 surveyed consumers said they had a confident understanding of their policy, when tested, their understanding of policy exclusions and limits was "poor".

The research confirmed that about 80 per cent of customers do not read a PDS before purchasing a policy.

Rather, the most commonly used sources of information for customers are online quotes, call centres and renewal letters, which are said to be "the most commonly used and highly rated source of information".

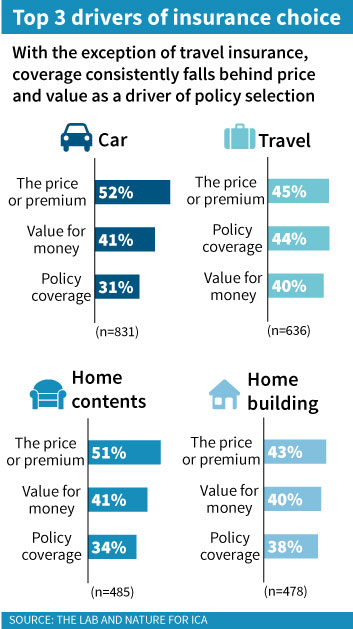

The task force also found that most consumers considered the price and level of cover as the only "detail" necessary to make an informed decision.

Other product features that consumers look for when deciding on a policy are coverage and exclusions, excess costs, competitive pricing, brand and good customer service.

In reviewing its results, the task force stated that the industry needed to do more "to ensure that consumers are not just focused on the price of a policy, but are ... selecting the right type and level of cover".

Insurance Council chief executive officer Rob Whelan said it was time to consider alternative methods to the PDS.

"The PDS will remain central to policy disclosure, but insurers are developing innovative methods to make them easier to search and digest," he said.

Senior solicitor for the Consumer Action Law Centre Philippa Heir said that ambiguity in the phrasing of a PDS often left consumers in the dark.

She pointed to Mr Wilson's situation, in which he was asked to show that he was employed immediately before falling sick.

"But what's 'immediately before'? If the weekend falls between the last week and the appointment with the doctor, what does that mean?" she said.

"I'm sure industry could simplify the language and the way a PDS is set out."

Solicitor for the Financial Rights Legal Centre Alexandra Kelly said standardising documents across industry would allow people to compare products side by side.

"We always have to have that lengthy document ... but we need to look at what technologies are available to better explain it."

The Insurance Council says it is working with members to develop "effective disclosure principles that are informed by the findings of the research".