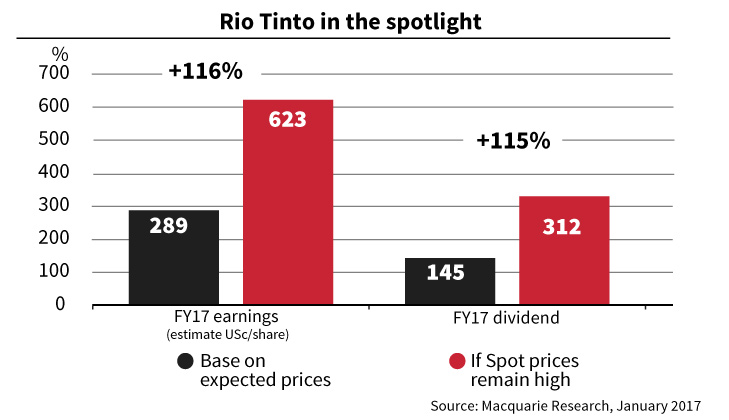

Enthusiasm for a share buyback from Rio Tinto at its upcoming results lends an optimistic note to the February earnings season, which could have more capital management surprises in store.

The danger is that investor expectations have already exceeded the willingness of boards to part with any spare cash, and the mood turns instead to one of disappointment. And good capital management is not just about shareholder rewards, it is also about debt.

More BusinessDay Videos

- Video duration

- 02:26

Australia calls time on commodity rally

Australia calls time on commodity rally

A commodities rebound thatâs seen iron ore and coking coal surge and boosted earnings at global miners is set to peak this year.

Up Next

Wall Street higher as Trump takes office

- Video duration

- 01:20

- Video duration

- 01:20

Wall Street higher as Trump takes office

Wall Street higher as Trump takes office

US stocks closed higher on Friday in a modest, but broad-based advance as Donald Trump was sworn in as US President.

Up Next

NAB admits security breach

- Video duration

- 00:41

- Video duration

- 00:41

NAB admits security breach

NAB admits security breach

The bank says human error was to blame when it sent details of 65,000 customers to the wrong email address in December.

Up Next

Netflix's decade of streaming

- Video duration

- 01:50

- Video duration

- 01:50

Netflix's decade of streaming

Netflix's decade of streaming

It's now been 10 years since Netflix made its most important strategic shift away from mail-in DVDs and into Internet streaming.

Up Next

Australia set to join global reflation

- Video duration

- 03:38

- Video duration

- 03:38

Australia set to join global reflation

Australia set to join global reflation

With inflation increasing in Europe, the UK, US and China, we address whether Australia will join this growing list and what could it mean for the RBA. (This video was produced in commercial partnership between Fairfax Media and IG Markets)

Up Next

Unemployment rate rises

- Video duration

- 00:26

- Video duration

- 00:26

Unemployment rate rises

Unemployment rate rises

In a surprise to economists, the unemployment rate in December rose to 5.8 per cent, from 5.7 per cent in November. Vision courtesy ABC News 24.

Up Next

China's first ballpoint pen

- Video duration

- 01:01

- Video duration

- 01:01

China's first ballpoint pen

China's first ballpoint pen

China produces about 38 billion ballpoint pens a year, but the country has never, until now, been able to produce its complicated tip.

Up Next

Gillard and Obama butt heads over Vegemite

- Video duration

- 00:57

- Video duration

- 00:57

Gillard and Obama butt heads over Vegemite

Gillard and Obama butt heads over Vegemite

Back in 2011, former prime minister Julia Gillard was asked about Vegemite while visiting a US high school.

Australia calls time on commodity rally

A commodities rebound thatâs seen iron ore and coking coal surge and boosted earnings at global miners is set to peak this year.

South32 is another stock that has been a target of speculation around boosted shareholder returns after it largely met production guidance despite a soft December quarter.

Mostly this atmosphere underscores the 180-degree swing in attitudes towards returning to capital to shareholders in the resources sector after billions of dollars was dusted on ill-timed projects and deals such as Rio's disastrous $US4 billion Riversdale Mining acquisition, of which around $US3.76 billion was later impaired.

The prospect of further buybacks on top of the cushion of dividends is a welcome safety net for an equity market now facing the test of how much of the Donald Trump optimism will be deliverable. The 45th president of the United States takes office on Saturday morning (AEDT) in Washington.

The problem with the reflation trade which lifted global equities last quarter is that nobody is sure whether the next wave brings good inflation – the kind where prices rise because of expectations of healthier growth and demand – or bad inflation, where prices rise because of negative trade policies.

Morgan Stanley is amongst those warning Australia's economy will be the collateral damage, not the beneficiary, of any trade war.

Celebration season?

All of that will play out over the next few years, but it is an important backdrop as local attention focuses will be on the February results season.

ASX 200 stocks are set to post their first year in three of earnings per share growth after two years of contraction, according to Credit Suisse, lifting the market's profit base by $10 billion to $100 billion.

Most of that is attributed to the recovery in commodity prices, and it is no accident that the best performing fund managers in 2016 held large positions in mining and energy stocks. Allan Gray's 38.1 per cent return last year when the median Australian equity fund tracked by Mercer returned 11.4 per cent was even more remarkable because it was ranked 96th out of 97 funds in 2015.

"There seems to be a lot of expectation for capital management this upcoming reporting season and that's great but those expectations are already built in. From here the risk is that capital management disappoints," Allan Gray's top stockpicker, Simon Mawhinney says.

"Some of these companies have much lower levels of debt and much higher levels of cash. Boards are generally reluctant to entertain large scale capital management initiatives, for one, it shrinks the company and the empire. Most company management and boards like to prevail over a growing empire not a shrinking one.

"When they do do it, it's usually a result of shareholder pressure and often of token proportions to appease an investment community."

And the fact is that there is still much volatility in the world to make boards cautious.

Volatile world

"The reality is that some decision made in China particularly around coal production has been the major driver of the windfall in cashflows," says Neil Boyd-Clark from Arnhem Investment Management.

'"How that cash gets deployed is still debatable. Whether it goes into dividends or developing new projects we'll just have to wait and see."

After all, China did announce this week it would can plans for 103 coal-fired power plants.

A buyback does not just raise earnings on a per share basis, lifting valuations – it also unlocks franking credits when they are available. But when share prices are high, buybacks are not thought to be a wise avenue of capital management.

"The issue with buybacks is typically they haven't been done at prices that are in the best interest of the company, buying back shares at the top of the cycle rather than the bottom of the cycle," says Boyd-Clark.

"Buybacks used appropriately are very effective."

The average Australian balanced super fund recorded a 7.7 per cent gain in the 12 months to December, research from Chant West shows.

Spotlight swings

Renewed interest in resources sector dividends takes the spotlight off the big four banks, which pay $20 billion a year back to shareholders collectively. The sustainability of that figure has been in doubt because the banking sector is regarded as both having passed the cyclical low point for bad debts, and offering almost nothing in the way of earnings growth.

Still the threat of new capital raisings to meet tougher regulatory requirements beginning in 2018 has softened lately. At best, that means the banks are likely to still need to top up their buffers, but perhaps now can do it without tapping investors for fresh equity.

While the banks have pedalled furiously to keep dividends stable – only ANZ has cut its dividend in dollar terms, by 7 per cent in May 2016 – resources sector dividends are climbing but do not tend to offer the same stability.

The origins of this are the painful lessons of what the big miners BHP Billiton and Rio liked to call progressive dividend policies: dividends that rose, or at a minimum stayed the same, every half-year even though earnings were see-sawing with commodity prices.

That thinking was abandoned only a year ago. Investors would recall that miners were scrambling to preserve their credit ratings at the same time because the nature of commodity prices means that when they are falling, leverage is rising. That brush with death is another reason why many analysts are declining to get carried away with capital management ideas in resources.

"Now you have this thing where the payoff profiles are skewed to the downside," Mawhinney says.

"The opportunities out there are vastly lower than they have been in the recent past. The stockmarket's high in the accumulation sense" – referring to the index including the value of reinvested dividends – "and there are few visibly cheap sectors in the stockmarket in our opinion." Energy would be the closest, but "the time to really buy those was a year or so ago."